COVID-19, the Fed and the markets, and a rat lesson

By Daken Vanderburg, CFA

Daken Vanderburg is Head of Investments for Wealth Management at MassMutual.

Posted on Oct 16, 2020

A Frenchman from the late 1800s, a man named Paul Doumer, taught us some very important lessons — ones worth bearing in mind when examining the latest turns of the COVID-19 crisis and the markets.

Doumer was an ambitious fellow. At the time, the French were squarely in their mode of expanding their global presence and colonizing various countries. Accordingly, Doumer arrived in Hanoi, the capital of Vietnam, in 1897 with the impressive-sounding title of Governor General of Indochina. Being an ambitious Frenchman, he seemed to feel it was his responsibility to make Hanoi into the capital of French Indochina, and accordingly….it needed to look the part. As such, Doumer went to work.

Over the course of a couple of years, Doumer tore down buildings and built new ones, organized neighborhoods, destroyed roads and built new streets, and generally ran Hanoi as the occupiers saw fit.

Doumer also believed that no city was truly civilized without a septic system, and therefore, installed an impressive sewer system underneath the city…particularly under the French Quarter.

Ahh, civilization was afoot! Unfortunately, underground sewer systems also tend to be a remarkable breeding ground for the common rat. Unintended consequence No. 1.

Soon enough, this impressive system created an equally impressive rat population, and government officials were now faced with a new problem. Not to worry, said the French, we can solve this. You see, the French realized that incentives drive behavior, and therefore, created incentives to encourage the removal of said rats.

Not only were the rats unsightly, they also carried the beginnings of what would become the bubonic plague. Yep, the rats had to go said the French. So, they offered a reward for each rat. First, they offered 1 cent per animal killed, then 2 cents in 1902, and 4 cents in 1904.

And, soon, the rat carcasses began to pore in, and the French congratulated themselves for such a clever scheme. During the first week of the program, nearly 8,000 rats were killed. As more people realized the incentives to killing rats were great, their methods improved, more impromptu hunters mobilized, and the process expanded. Fast forward two weeks, and nearly 4,000 rats were being killed each day. Two more weeks, and the numbers jumped to over 15,000 per day.

And this is where the story gets interesting…

With so many rat carcasses, the French authorities made a minor modification. They began to just ask for delivery of the rat tails…clearly the carcasses are not necessary. Soon enough, hunters figured out that removing tails was much more humane (and easier) than killing the entire rat, and Hanoi citizens began to see rats running around Hanoi without tails.

Unfortunately, the rat population continued to increase. How could this be, wondered the bureaucrats? Clearly the French had understood incentives and had incentivized appropriately, right?! Well, yes, but they hadn’t thought through the unintended consequences of their policy.

Soon they realized that the more enterprising Hanoi citizens had set up rat farms on the outskirts of the city. The farmers reasoned “why should I run through the disgusting city sewers catching rats, when I can produce many more in my own backyard?” This is the lesson of unintended consequences.

As such, for today, we will provide an update on COVID-19, and then turn to a more present-day discussion of unintended consequences: The U.S. Federal Reserve.

Let us begin…

COVID-19

Let me first acknowledge I have received several calls and emails this week highlighting how COVID-19 case count in New Mexico is out of control, or Wisconsin is spiraling, or a certain county has changed. While there is much truth to those statements, I want to make clear that I am focusing on the law of large numbers. I tend to focus on the entire United States, or the entire world, because I believe it makes us less likely to be distracted by hot spots, and more aware of the larger trends.

Therefore, let us zoom out for our perspective. As we tend to invest in the entire United States economy, we try to provide perspective for the entire country.

For purposes of brevity, let me summarize this following section as very little has changed. Absolute numbers are still quite high, and the growth rate of cases has fallen dramatically, but has recently steadied out. With that short lens in mind, the virus is not winning, and yet neither are we. We are, in the short term, coexisting.

As of Oct. 15:

There are now more than 38 million people worldwide that have had confirmed COVID-19 infections (roughly half of 1 percent of the world’s population).

There are now more than 7.8 million Americans that have had confirmed COVID-19 infections (roughly 2.2 percent of the United States population).

There have been more than 1 million deaths attributable directly to the COVID-19 virus worldwide, with more than 220,000 of those from the United States.

With that said, the growth of those cases (which I believe the market is focused on) remains steady (it is worth noting there is an increase in the last couple of days that we are watching closely).

For the first perspective on this dynamic, let’s start with Chart 1 which shows global cases, and the global growth rate.

The blue line is the total number of global cases (now more than 30 million) and corresponds to the left axis. The grey line is the growth rate of those cases and corresponds with the right axis. Thankfully, the growth rate has come down (and stayed down) since the peak in March when it was unsustainably high. Again, it is worth nothing there is a slight uptick in growth rates over the past couple of days. While it is too early to determine if this is the beginning of something more material, we are watching the data closely.

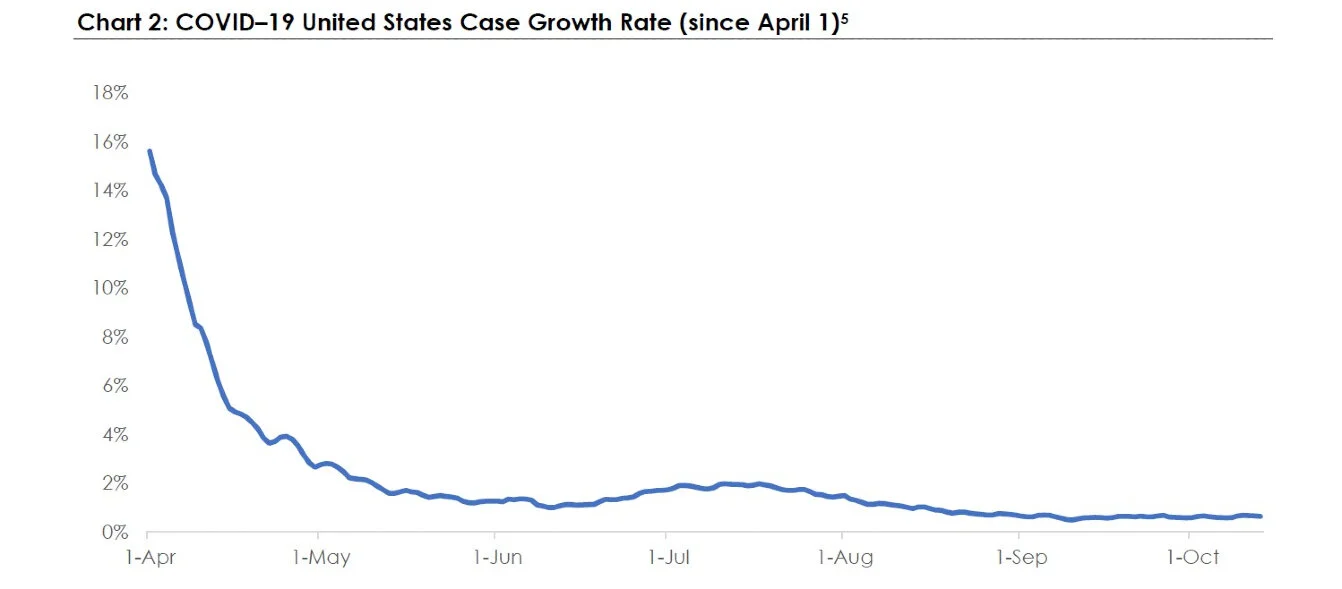

Domestically, Chart 2 demonstrates the growth rate of cases in the United States alone.

As a reminder, back in March, when COVID-19 was spreading rapidly, case growth in the United States was growing by more than 30 percent per day, which was both terrifying and unsustainable. We, as a society, made changes, and growth rates fell to the mid-teens in April, down to 2 percent in June, and now, U.S. COVID-19 cases remain roughly 0.6 percent per day (on average).

The growth rate was very high in early April, then fell very quickly, then rebounded a bit toward the beginning of July (as growth in the South exploded) and remain steady (roughly 0.64 percent on a five-day smoothed basis).

Chart 3 takes the very same data and converts it to the number of days to double the cases in the United States. I continue to find this is a more intuitive way to understand how fast cases are changing, and as can be seen, is demonstrating the slight increase in case growth in recent days.

The chart largely follows the story of the United States. In late March, the U.S. was in complete lockdown as case growth was largely out of control. At that point, the U.S. was doubling cases every three to five days. We learned, we evolved (and no, not quickly enough), but we nonetheless improved to late May and early June where we were doubling cases every 64 days.

The South then began to reopen, and many states pushed back entirely on some of the government guidelines. Growth rates increased again, and the days to double fell to 37 days on July 13.

Fortunately, over the past six weeks, we have remained between 110 and 125 days to double the number of cases in the United States. While this is clearly higher than we would all prefer, it at least provides some optimism that we are co-existing and experiencing more normal lives (at least relative to the depths of the shutdown).

Economic update

We in the finance industry love to make things confusing. It makes us feel important and all-knowing somehow. I’m halfway through my day, and so far, today I have seen the terms CPI, PCE, QE, velocity, stimulus, easing, M1, M3, credit expansion, hawkish Fed and dovish Central Bank.

Yet because the concepts matter (even though the abbreviations don’t), let’s start with a couple definitions.

Imagine for a moment, you are marooned on an island with 10 other people. The island produces one good and one good only: bananas. So, you harvest bananas, and you eat bananas. But one day, one of your island mates can’t find bananas and so would like to buy your bananas with the shiny rock they found. Sure, you say … but how many bananas for that shiny rock? Well, let’s assume there are 10 bananas on the island, and there are 10 shiny rocks. Seems reasonable that each banana would cost one shiny rock. Great. Dear reader, you now understand the theory of money.

Now imagine that an enterprising island mate of yours digs around one day and finds 10 more shiny rocks. Therefore, island inventory is now 10 bananas and 20 shiny rocks. Earlier, we had 10 bananas and 10 shiny rocks, so the price of a banana was established as one shiny rock. Now, we have the same number of bananas, but twice the number of shiny rocks, so the price of a banana should now be two shiny rocks. Dear reader, you now also understand inflation.

Inflation is nothing more than how the price of a good (or a basket of goods) changes. In our prior example, the price of bananas went up a lot, which is just another way of saying inflation was high.

This then sets the groundwork for returning to our lesson from the Hanoi rats: Unintended consequences.

Just as on our fictitious island, in the United States, the number of shiny rocks (also known as dollars) also can change. In fact, with just the click of a button, the Central Bank (known in the U.S. as the Federal Reserve) can create trillions more dollars. That’s right … just as our enterprising friend found more shiny rocks, the Federal Reserve has instantaneously created more dollars.

Let us now turn to Chart 4 to help understand just how many dollars have recently been produced.

This chart tells a pretty interesting story, namely that the Fed has begun using a tool that it never used before. Rewind this chart back 60 years and there’s not much to see. During the last two crises (primarily in 2007-08, and then again, this year), the Fed has printed several trillion dollars each time to provide liquidity and help markets stabilize. We have gone from less than $1 trillion in 2002, to more than $7 trillion today. For context, remember our entire economy is around $21 trillion.

Were these the right decisions? I think the short answer is, during the crisis, the action clearly treated some of the symptoms, and did so quite directly. Over the long term? I’m not sure.

Remember the story of the Hanoi rats. Incentives drive behavior, yes, but there are always unintended consequences. In this context the Federal Reserve has driven down interest rates, but mortgage borrowing has surged, and home prices have been remarkably stable and encouraged additional purchasing. The Federal Reserve plugged the holes in the system during the most recent crisis, and did so quite well, but they also have encouraged additional risk-taking, and have created a perception that the Federal Reserve will always be there as a buyer of last resort.

To be clear, I was quite impressed with the speed and accuracy the Federal Reserve injected liquidity into the markets in this recent market crisis. They treated exactly what needed to be treated, and they did it quickly and surgically. Yet each action can have a reaction, and often can have many reactions. We just aren’t sure what they always will be …

So, therefore, with that knowledge, what are we to do?

First, it is therefore incumbent upon us to strive to build portfolios that can sustain whatever market moves are to come. While there are no perfect portfolios, we can and should strive to build those that are thoughtfully constructed for the various types of environments we are likely to face. For example, while bonds are clearly still attractive instruments for trying to reduce the volatility of a portfolio, most bonds are generally not providing much yield. This means we must find other sources of returns to provide yields, as well as additional sources to further reduce the risk of our portfolios.

Second, we must be thoughtful and careful about how much risk we should really take. I would argue there is as much risk now as there ever has been and, given how optimistic the market has been, I would argue there is more risk to the downside.

Third, we should use the periods like March to serve as a barometer for our own emotional makeup. Behaviorally, we all state we want more return and are willing to endure the risk, but then we may have a very difficult time during the more severe market declines. Let us use this emotion as a barometer to gauge if we have too much risk. Thoughtful planning, saving, and portfolio construction should largely allow us to ignore the gyrations of the market … and if we are actively and visibly shaken during market declines, we likely have too much risk.

And lastly, stay safe, and turn off the investment news channels.

______________________

1 https://realhistory.co/2018/10/11/great-hanoi-rat-hunt/

2 https://www.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6

3 Sources: Bloomberg, World Health Organization as of Oct. 14, 2020

4 https://www.worldometers.info/coronavirus/country/us/

5 Sources: Bloomberg, World Health Organization as of Oct. 14, 2020

6 Sources: https://www.worldometers.info/coronavirus/country/us/, as of Oct. 14, 2020

7 Sources: https://fred.stlouisfed.org/series/WALCL as of Oct. 14, 2020

8 Sources: https://www.bea.gov/news/glance