December 2024 - Animal Spirits

By: Kyle M. McBurney CFP

Managing Partner at Highland Peak Wealth

Following Trump’s surprise election win in 2016, markets surged on the promise of lower taxes, deregulation, and infrastructure spending. I still remember a former colleague leaning back in his chair, proclaiming, “Looks like animal spirits are back.”

Animal Spirits? Huh?

Simply put, “Animal Spirits” is a term coined by economist John Maynard Keynes, describing the emotions and instincts that drive human behavior in markets. Sometimes referred to as "gut instinct," animal spirits emerge when logic and math take a backseat to optimism, fear, and the urge to do something. Think of the euphoria driving 2021’s market craze or the panic-stricken bank run handled by George Bailey in It’s a Wonderful Life (a must watch in my household).

Still, with a tremendous November for markets in the rearview, markets are in an undeniable uptrend. Momentum is back in the driver’s seat.

The recent election, with echoes of 2016, has sparked renewed optimism about increased investment, dealmaking, and potential reforms in government spending. Markets have responded enthusiastically: stocks are up, bond yields have fallen, and the dollar has strengthened across most currencies—except Bitcoin, which remains in its own category of unique exuberance.

Stocks delivered impressive gains in November, with the Dow and S&P 500 marking their best monthly performance of 2024. Small caps also enjoyed a fantastic month, with the Russell 2000 surging nearly 11%. Despite some sectors, like autos, facing pressure from Trump’s tariff rhetoric, equity traders largely brushed off these concerns, focusing instead on the broader market rally.

As December begins—a historically strong month for stocks—investors are hopeful for a continued rally to close out a year in which the S&P 500 has already climbed a remarkable 26%. In the bond market, per Bloomberg, the 10-year Treasury yield eased to 4.192%, with attention now turning to upcoming economic data, including construction spending and the November jobs report. While optimism runs high, Federal Reserve officials have signaled caution, suggesting rate cuts could pause if inflation progress stalls. Markets are balancing hopes for rate cuts with concerns about inflation as they move into the final stretch of the year.

It is not lost on us that this is the first newsletter following the election. We recognize that within our readership there is a mix of excitement and anxiety. These are all normal emotions for this post-election period. Like all things, this too shall pass.

For those optimistic about market momentum, a tempered outlook, in our view, is wise—early days of any presidency are often filled with hope, but the real test comes when policies meet reality. For those concerned about political change, staying the course and avoiding emotionally driven investment decisions is key.

At Highland Peak Wealth, we’re focused on guiding our clients through both the highs and lows of animal spirits. While markets have delivered extraordinary gains, history reminds us that emotions can turn quickly. The year 2022 is our most recent reminder of excessive optimism turning into anxiety very quickly. Our priority is to help you stay grounded and aligned with your long-term goals, no matter where the headlines or markets take us next.

A Look Back at the “Trump Trade”

It’s been less than a month, but let’s check in on the Trump playbook that we previously communicated.

How are those themes working? To summon my inner Larry David, pretty pretty prettyyy good.

As a reminder, our team had targeted a handful of post-election investment themes on the equity side –

1) A Rally in Small Cap Stocks

2) Sector Rotation – Banks, Tech, Energy

3) US Stocks over International Stocks

Let us quickly look at each.

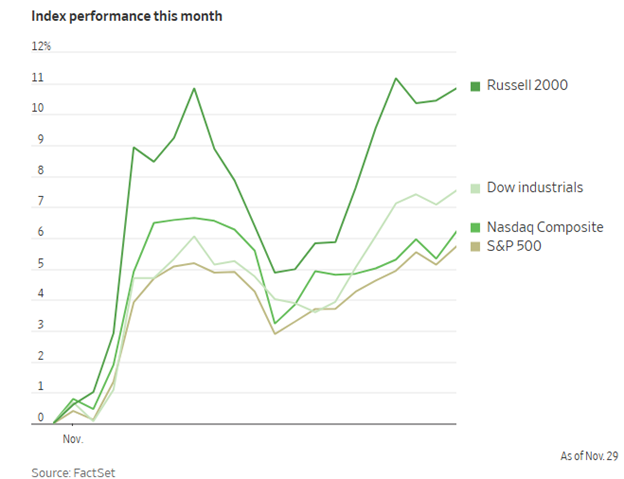

Small Cap Stocks Surging

Is this the long-awaited small-cap rally? Since the election, small-cap stocks have surged an impressive 10% for the month, leaving other indexes in the dust. The chart below highlights how small caps have pulled ahead, capturing the market's attention:

Optimism for small caps is rising, driven by expectations that Trump’s protectionist trade policies and deregulation will benefit smaller domestic companies. Combined with lower interest rates and potential tax cuts, and you have a promising cocktail that might keep small cap growth humming in early ’25.

Still, history shows small caps surged after Trump’s 2016 win but underperformed much of 2017. This is yet another reminder for the need to balance enthusiasm with caution.

Sector Rotation

At the sector level, investors appear to be re-engaging in the successful trades from the post 2016 election – banks, tech, and energy stocks. Per Koyfin, here is their performance since the election (11/3/24 – 12/3/24):

Banks: 8.17%

Energy: 7.36%

Communications: 8.24%

Tech: 5.76%

So far, so good as the above sectors represent four of the top six best performers last month (Consumer Discretionary and Industrials are the other two).

Why are we interested in these sectors following the election? Here are some quick thoughts –

The possibility of lighter/looser regulation may boost lending

Potential for a resurgence in dealmaking

Small business growth may boost lending opportunities for regional banks.

The possibility of lighter/looser regulation may boost lending

Potential for a resurgence in dealmaking

Small business growth may boost lending opportunities for regional banks.

The possibility of lighter/looser regulation may boost lending

Potential for a resurgence in dealmaking

Small business growth may boost lending opportunities for regional banks.

Our interest in these sectors is not set in stone. As new information emerges, we’ll adapt accordingly. After all, history has shown how unpredictable market leadership can be under a new administration, making flexibility key. Nonetheless we are off to a good start but watching closely as we enter the new year.

USA vs. International

Geez, where do we even begin?

For nearly two decades, U.S. stocks have been the undisputed leader, making the case for geographic diversification a tough sell. Beyond the BRICs (Brazil, Russia, India, and China) thriving in the late 2000s and early 2010s, international equities have struggled to add meaningful value to portfolios. While there have been brief bright spots—2017 and 2022 most recently—they’ve been short-lived and far from any tradeable trend that we can act on.

Source: Strategas

That divergence has only widened in 2024. The S&P 500 is up a remarkable 27% year-to-date, while the MSCI EAFE Index, tracking developed markets outside the U.S., has managed only a 6% gain. Emerging markets, buoyed by strength in India (a country we have been very interested in), have fared slightly better at 7.5%.

This kind of gap is rare, but it certainly highlights why a tilt toward U.S. markets has been the winning strategy for investors so far. As you can see, this divergence has only increased over the past three months.

The post-election split is noteworthy. U.S. growth prospects have boosted domestic markets, while the threat of tariffs and geopolitical uncertainty weigh heavily on international equities.

It is concerning that developed markets are grappling with unrest, from the French government teetering on collapse to South Korea’s brief declaration of martial law. These events, combined with ongoing conflicts in Ukraine and the Middle East, leave little room for optimism abroad.

Looking outside the US, it’s hard to get overly excited. As such, we think it is wise to maintain a preference for US stocks. This theme will not last forever, but while we are looking and deeply hoping for a trend to emerge, we are just not seeing anything yet.

That said, international equities won’t remain out of favor forever. Valuations are becoming more attractive, and history shows that cycles of U.S. outperformance don’t last indefinitely. Since 1975, according to Bloomberg and Hartford Funds, such cycles have averaged eight years, and we’re now 13.6 years into the current streak, based on rolling 5-year monthly returns.

In fact, want to take a guess as to what asset classes performed best in 2017, in Trump’s first year? Well, that would be Emerging Markets stocks (up 37.8%) with Developed International stocks in second place (returning 25.6%), per JP Morgan.

If nothing else, it is a reminder not to entirely give up on international equities; their time will inevitably come.

In Summary

The Trump playbook has certainly delivered so far, and we’re pleased with how those adjustments have played out. It recalls a scene from 300, where a captain, having repelled wave after wave of Persian forces, exclaims, “Hell of a good start!” after day one of the Battle of Thermopylae.

Hell of a good start, indeed!

But, as history often reminds us, early success doesn’t guarantee the future.

A glance back at Trump’s first term is proof. Many of the themes that worked well initially—like energy and financials—fizzled by the end. Ironically, sectors like banks and energy performed better under Biden than Trump.

Go figure!

Of course, a global pandemic added a ho-hum twist, but it’s a reminder that presidents have far less control over markets than we sometimes imagine.

The Federal Reserve, for example, will continue to move markets as we approach 2025.

Fed Talk

Markets have been as jolly as ever this week, with the odds of a Fed rate cut adding to the holiday cheer.

Stocks rallied after Fed Governor Christopher Waller hinted, he’s leaning toward a rate cut at the December 18 meeting, citing progress on inflation. According to the CME FedWatch Tool, the chance of a cut has climbed to 77%, up from 65% earlier in the week. Looks like Santa might not be the only one delivering gifts!

Meanwhile, holiday spending is off to a flying start. Per Mastercard reporting, Black Friday sales rose 3.4% year-over-year, with a sleigh-full of growth coming from a 14.6% surge in online sales, while in-store shopping stayed flat. Cyber Monday is set to keep the spirit alive, as consumers embrace discounts with plenty of holiday enthusiasm.

Not exactly behavior you'd expect from a crowd worried about recessions, right?

This week, the Fed will be closely eyeing key data points, including Wednesday’s ADP employment report and Friday’s November jobs numbers. Powell and the team know labor market strength will be a major factor in deciding whether to hit pause—or end the year with another rate cut. Looking ahead, 2025 rate cuts are still expected, with some forecasts, like Bank of America’s, projecting a 25-basis-point cut in both March and June before the Fed takes a breather.

Expect an outlook on rates in next month’s Trail Guide.

Chart of the Month – Election-to-Inauguration Rally—Followed by Post-Inauguration Turbulence

Source: Strategas

Bonus Chart – The Sweet Spot for Stocks: Mid-November to Mid-January’s Seasonal Strength

Source: Strategas

Allocation Update

As we enter what has historically been the best stretch of the year for stocks, the trend remains bullish—and so are we. That said, let’s be clear: the U.S. stock market is undeniably expensive by historical standards.

Need proof? Take a look at the Shiller P/E Ratio.

Named after economist Robert Shiller, this tool helps evaluate whether the market is overvalued, undervalued, or fairly priced. Last week, the S&P 500 reached its second-highest reading on record for the Shiller P/E Ratio, surpassing the levels seen in 2021.

The only time it’s been higher than today’s reading? The dot-com bubble of 1999–2000.

In our view, these elevated valuations, combined with structural fiscal challenges and increasingly exuberant investor sentiment, make a case for approaching the market with balance and caution. While we expect the current momentum to carry us into the end of the year, we’re also mindful of that pesky voice in the back of our minds: “Can this really keep going?” Bull markets don’t die of old age, but valuations at these levels give us reason to pause and reflect.

As we head into the holiday season, we’ll spend considerable time sharpening our 2025 outlook. For now, our focus remains clear: maintaining quality, managing risk, and positioning portfolios for sustainable, long-term growth.

Here's a snapshot of our perspective:

Equities – Overweight Approach:

U.S. Stocks Still Preferred: Our inclination towards U.S. equities over international markets has only increased in ’24.

Small Caps Rallying? Small-cap stocks have been impressive of late and have benefited by rate cuts and election. More to come?

Developed International: Some serious, and growing, political and geopolitical risks give little room for optimism.

Fixed Income – Underweight:

Core Bonds: While rates have fallen, Trump policies could push rates higher. We remain balanced and are taking a “wait and see approach” regarding tilting towards short or longer dated bonds.

Floating Rate Bonds and CLOs: Yields remain strong, but a closer look is warranted as rates fall.

Alternatives – Neutral

Gold Overweight: As with stocks, Gold had a strong ’23 and is enjoying a fantastic ’24

Growing Interest in Private Alternatives: Where applicable, our team expects to utilize private investments more meaningfully moving forward.

Cash – Neutral

Strategic Use of Cash: Yields have become less attractive as rates fall and equites has become more enticing.

As we approach the end of the year, our team at Highland Peak Wealth is here to assist. Whether it’s last-minute gifting, charitable contributions, tax payments, or required minimum distributions (RMDs), we’re ready to help. Don’t hesitate to reach out.

I write this newsletter feeling a few pounds heavier— a curious mystery given my commitment to "vegetables" like carrot cake, zucchini bread, and pumpkin pie. Thanksgiving was a whirlwind of food, family, and friends, but as soon as the clock struck midnight on Thursday, Heather and the kids wasted no time launching into full December holiday mode.

Already, the lights are up, the tree is decorated, and our sugar intake has spiked. Hanging those stubborn lights on the roof? A clear reminder that life insurance and disability insurance are never a bad idea.

From all of us at Highland Peak Wealth, we wish you and your family a safe and joyous holiday season.

Here’s to a healthy and prosperous 2025!

And for those already thinking about New Year’s resolutions, take a cue from Calvin & Hobbes.

Kyle M. McBurney, CFP®

Managing Partner

The opinions expressed herein are those of Kyle McBurney, CFP as of the date of writing and are subject to change. This commentary is brought to you courtesy of Highland Peak Wealth which offers securities and investment advisory services through registered representatives of MML Investors Services, LLC (Member FINRA, Member SIPC). Supervisory office: 280 Congress Street, Boston, MA 02210. (617)-439-4389. Highland Peak Wealth is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Past performance is not indicative of future performance. Information presented herein is meant for informational purposes only and should not be construed as specific tax, legal, or investment advice. Although the information has been gathered from sources believed to be reliable, it is not guaranteed. Please note that individual situations can vary, therefore, the information should only be relied upon when coordinated with individual professional advice. This material may contain forward looking statements that are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. This material does not constitute a recommendation to engage in or refrain from a particular course of action. Referenced indexes, such as the S&P 500, are unmanaged and their performance reflects the reinvestment of dividends and interest. Individuals cannot invest directly in an index.

Glossary of Index Definitions

Indexes are unmanaged, do not incur fees or expenses, do not reflect any deduction for taxes, and cannot be purchased

directly by investors.

The S&P 500® Index is a widely recognized, unmanaged index representative of common stocks of larger capitalized U.S. companies.

The S&P Muni Bond Index is a broad, market value-weighted index that seeks to measure the performance of the U.S. Municipal bond market.

Dow Jones Industrial Average is a price-weighted average of 30 actively traded Blue Chip stocks, primarily industrials, but also including other service-oriented firms; may be used as a benchmark for large cap stocks

NASDAQ Composite is a broad-based index of over 3,000 companies, which measures all domestic, and non-U.S.-based common stocks listed on the NASDAQ Stock Market, Inc.

The NASDAQ 100 U.S. Index is a composed of the 100 largest, most actively traded U.S. companies listed on the Nasdaq stock exchange.

The Russell 2000® Index is a widely recognized, unmanaged index representative of common stocks of smaller capitalized U.S. companies.

The MSCI EAFE Index is a widely recognized, unmanaged index representative of equity securities in developed markets, excluding the U.S. and Canada.

The MSCI Emerging Markets (EM) Index is an unmanaged market capitalization-weighted index of equity securities of

companies domiciled in various countries. The Index is designed to represent the performance of emerging stock markets

throughout the world and excludes certain market segments unavailable to U.S.-based investors.

The MCSI All Country World Index (ACWI) captures large and mid cap representation across 23 Developed Markets and 24 Emerging Markets.

The Barclays U.S. Aggregate Bond Index is a broad measure of the U.S. investment-grade fixed-income securities market.

The Bloomberg U.S. Aggregate Bond Index is an unmanaged index of fixed-rate investment-grade securities with at least one year to maturity, combining the Bloomberg U.S. Treasury Bond Index, the Bloomberg U.S. Government-Related Bond Index, the Bloomberg U.S. Corporate Bond Index, and the Bloomberg U.S. Securitized Bond Index.

The Nikkei Index is a price-weighted index composed of Japan’s top 225 blue-chip companies traded on the Tokyo Stock Exchange.

©2023 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its

content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information